What’s up, fellow market follower?

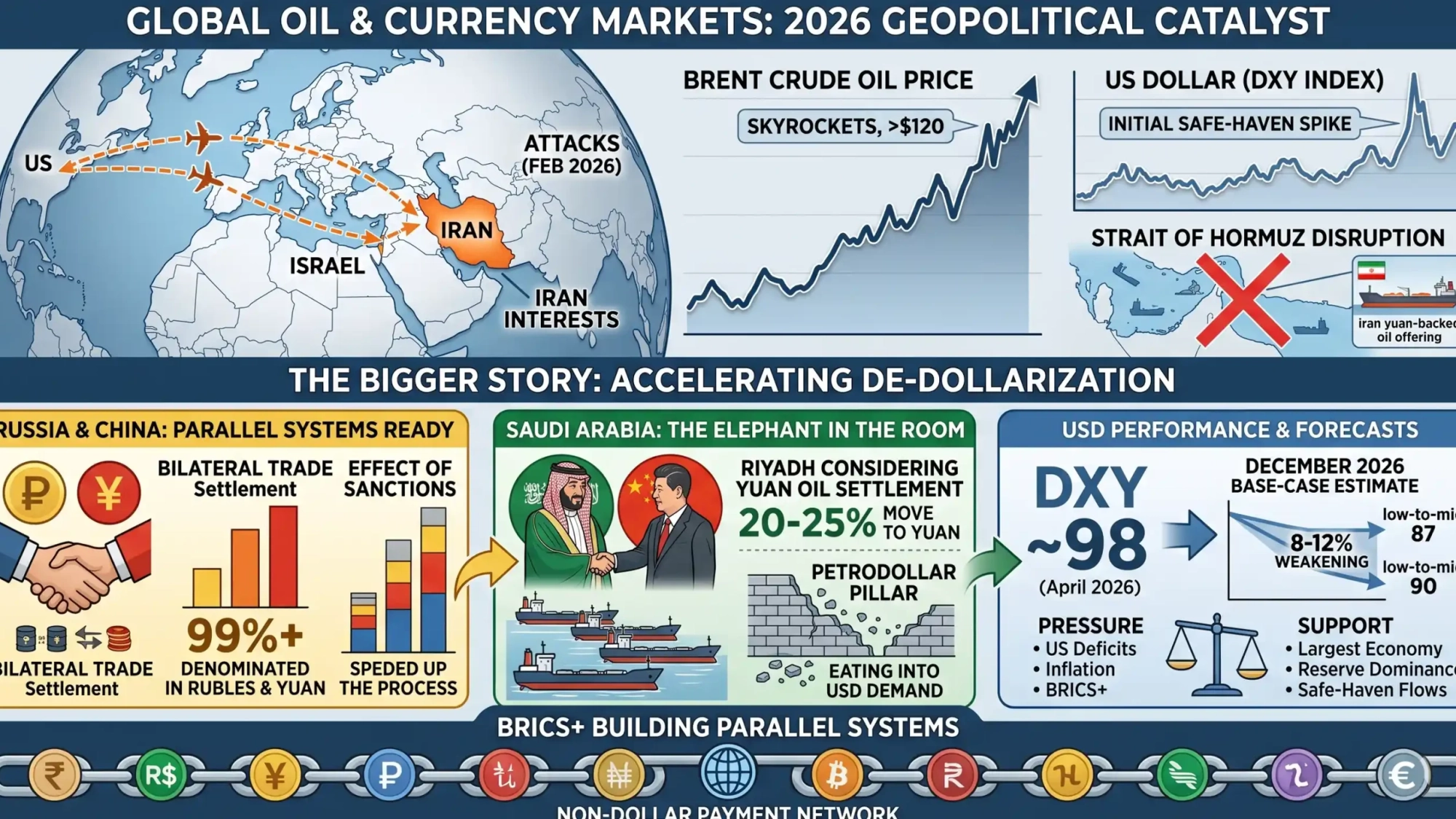

If you have been reading up on the latest news these past few days or weeks, then you probably understand what we’re talking about here. The attacks carried out by the US and Israel on Iran starting from late February 2026 not only disrupted the region, but also caused a stir within global oil and currency markets. Oil prices skyrocketed while the US dollar was temporarily buoyed by safe-haven demand. However, beneath the headlines lie the bigger story: nations are speeding up their de-dollarization efforts.

In fact, monitoring the currency market and geopolitics over the last 15 years gave me an idea that this time around, things will be a little bit different from the previous flare-up. Indeed, it is going to be the catalyst to accelerate something that economist have been predicting for years: the de-dollarization process. The result is quite realistic and within December 2026, the USD may become weaker for about 8-12% compared to its current position on the global market.

Now let’s dive into the reasoning behind my assumptions and explore some facts and figures that will explain how this situation can take place and why you do not need to run for cover just yet.

The Clash That Turned the Tables

As soon as US and Israeli troops attacked Iranian interests at the end of February, what happened next was typical: oil prices jumped up (with Brent hitting $120), the Strait of Hormuz saw shipping traffic fall off sharply, and investors scrambled to buy dollars to hedge their bets. The DXY index wavered between 98–100 in March but settled at about 98.2 by mid-April 2026.

However, there was another side to the story that was mostly overlooked in all the noise. It wasn’t just that the conflict boosted the short-term value of the dollar; it called into question the very existence of the petrodollar regime. According to news reports, Iran started offering safe passage through the Strait of Hormuz on the condition that the transaction be conducted using yuan-backed oil.

Russia & China: Both De-Dollarized and Ready to Go!

For quite some time now, Russia and China have been developing their own systems. And by the end of 2025, they have managed to redirect their 95% of bilateral trade out of the dollar. As of today, the ratio stands at over 99%, denominated in rubles and yuan.

Sanctions? Well, they only sped up the process but didn’t stop it. The problem is that Russia needs to continue using Chinese currency to survive, while China gains more power over the yuan without making it fully convertible (which is one of their goals).

This is not something marginal anymore.

The Elephant in the Room – Saudi Arabia

This is where it gets exciting. Saudi Arabia has always been the pillar of the petrodollar, with the vast majority of its oil priced and settled in USD. However, the Iran issue has suddenly brought the subject up.

There have been reports indicating that Riyadh (and other Gulf states such as the UAE) are seriously considering paying for their oil shipments to China in yuan, or even beyond, if it will ensure free passage through Hormuz or reduce dependence on the U.S. dollar payment system. A 20-25% move to yuan settlements from Saudi Arabia alone towards China will rock the world. Not because the dollar is finished tomorrow, but because it will start eating into the main source of its demand.

So… How Much Could the Dollar Actually Fall by December 2026?

Let’s be realistic and data-driven — no fear-mongering.

- The dollar already lost roughly 10% in 2025 — its worst year since 2017.

- Year-to-date 2026 has been volatile but net negative so far.

- Consensus forecasts from major banks point to a DXY range of roughly 90–97 by year-end, with a bias toward the lower end if de-dollarization momentum builds and the Fed eventually cuts rates.

My base-case estimate: An additional 8–12% weakening from current levels (~98) by December 2026. That would put the DXY in the low-to-mid 87–90 range.

Why this range and not a doomsday 20–30% crash?

- The US economy is still the world’s largest and most liquid.

- The dollar remains the dominant reserve currency (still ~58% of global reserves).

- Central banks can’t dump dollars overnight without crashing their own portfolios.

- Short-term safe-haven flows during crises still favor the greenback.

But the pressure is real: higher US deficits from war spending, sustained high oil prices feeding inflation, and BRICS+ nations actively building parallel payment systems all point to gradual but persistent downward pressure.

Leave A Comment